The State Bank of Pakistan (SBP) has released a set of four guidelines around green financing mainstreaming in Pakistani banks. The three earlier frameworks; Green Banking Guidelines (GBG), ESRM, and Pakistan Green Taxonomy (PGT), all have a distinct focus, but they are designed to be mutually reinforcing. Together, they address different facets of the challenge: strategy & governance (GBG), risk management (ESRM), and asset classification & transparency (PGT):

- Green Banking Guidelines as the Umbrella: The GBG serve as the high-level policy umbrella under which the other two frameworks operate. They set the vision and holistic scope, covering risk management, business opportunities, and internal footprint. Think of GBG as “what banks should strive to do in sustainable banking.” Within that, it called for environmental risk management procedures and green business facilitation – which are the areas that the ESRM manual and the PGT now elaborate on. In fact, SBP developed the later frameworks to flesh out the GBG: the ESRM manual establishes standardized procedures to achieve the risk management objectives of GBG, and the PGT provides criteria to achieve the green financing and reporting objectives of GBG. Without GBG, the ESRM and PGT would lack a unifying policy context; conversely, without ESRM and PGT, the GBG would remain broad principles without concrete tools.

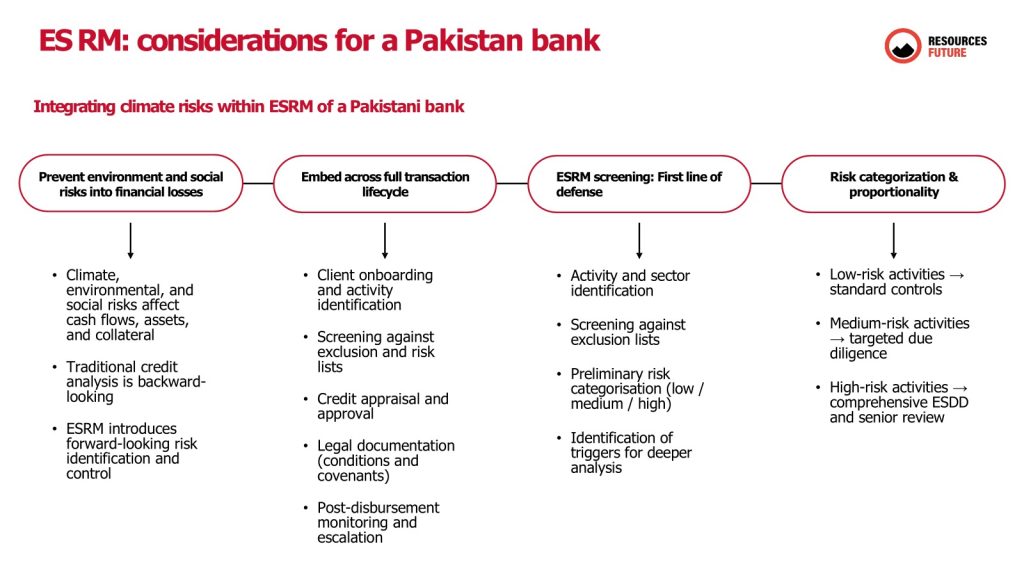

- ESRM as the Risk Management Fulfillment of GBG: The ESRM framework is essentially the implementation mechanism for the risk management pillar of GBG. SBP itself stated that the ESRM manual is meant to ensure compliance with the GBG’s risk management expectations. By adopting the ESRM system, banks can credibly answer the GBG’s fundamental question: “Do we have credible systems to identify and manage E&S risks?” (one of the key governance questions for effective GBG implementation). The processes defined in ESRM, from client onboarding screening, to risk categorization (low/medium/high), to E&S due diligence for high-risk cases, all enable early identification and control of environmental and social risks. This complements GBG’s intention that banks move from reactive, back-end checks to proactive, front-loaded risk management. For example, GBG expects that high-risk transactions are escalated early to senior management. ESRM provides the workflow (screening and categorization triggers) to make that happen: a transaction flagged as High E&S Risk would require senior credit committee review and risk mitigation plans before approval. ESRM embeds a “first line of defense” for E&S risks into the bank’s overall risk framework.

- PGT as the Business and Transparency Fulfillment of GBG: The PGT complements the business facilitation and reporting aspects of GBG. GBG called for banks to actively finance green projects and develop green products; PGT now gives clarity on what counts as “green” in that context. This guides banks in setting their green finance priorities and targets. For instance, a bank updating its Green Banking Policy (per GBG) is now advised to reference the PGT for defining priority sectors. The taxonomy’s existence encourages a more strategic and disciplined approach to green business, instead of opportunistic deals: banks can systematically identify sectors from the taxonomy and build expertise/products in those areas, rather than doing one-off “green” deals that lack strategic focus. Moreover, PGT enables consistent reporting of green portfolios to SBP and the public. Under GBG, SBP intended to monitor green investments by banks; PGT provides the standard to measure that. Without PGT, one bank’s “green loan” could be another bank’s “neutral loan”, now everyone is on the same page, much like the EU’s Green Asset Ratio concept. This consistency also feeds back into risk management: PGT-aligned reporting can reveal a bank’s exposure to high-carbon vs. green assets, which is useful information for managing transition risk (the risk of asset value loss due to the economy transitioning to low-carbon). In future, SBP or banks themselves might set targets like “X% of portfolio in taxonomy-aligned green assets by 2030,” linking to national climate goals.

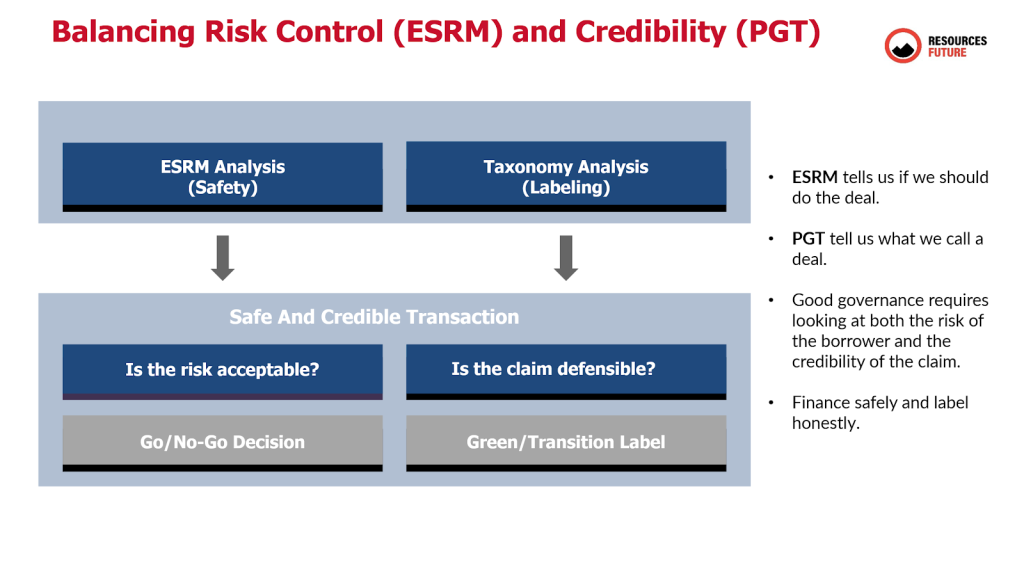

- Ensuring No Conflict and Mutual Reinforcement: It’s important to note that the taxonomy’s Do No Significant Harm and social safeguards criteria align with ESRM’s requirements. For example, PGT will deem an infrastructure project green only if it does not cause significant environmental harm and meets social safeguards. How does a bank ensure that? By conducting a proper E&S risk assessment per the ESRM framework. If the ESRM process finds, say, that a hydro project could severely impact a local community’s livelihood without adequate mitigation, that project might fail the DNSH test of the taxonomy. Thus, ESRM acts as the gatekeeper to prevent greenwashing, it will ensure that projects labeled green truly adhere to environmental and social standards. Conversely, the taxonomy gives ESRM a forward-looking, positive use: not only can banks use ESRM to avoid negatives, but also to identify which high-risk projects, if well managed, could count as green and attract investment.

- Holistic Governance and Strategy: Implementing all three frameworks in unison leads to a more holistic governance approach. GBG set up the requirement for governance structures (e.g. Green Banking Champions, units, and board oversight). With ESRM, those governance structures have concrete risk data and escalation pathways to act upon (e.g. a Sustainability or Risk Committee gets regular ESRM risk reports). With PGT, the same governance bodies can also oversee green business performance and ensure credibility of any green claims (avoiding a “credibility failure” or accusation of greenwashing by sticking to taxonomy definitions). In essence, GBG is the broad governance umbrella, ESRM is integrated into the bank’s three lines of defense on risk (first line business units, second line risk management, third line audit), and PGT provides a strategic direction for growth and disclosure.

In simpler terms, one can say GBG is the “why and what”; why we need to go green and what areas to cover; ESRM is the “how” – how to manage risks and avoid pitfalls along the way; and PGT is the “where” – where to focus investments for environmental impact and how to measure them.

Current State of Implementation in Pakistani Banks

Implementing these frameworks across Pakistan’s banking sector is an ongoing journey. As of early 2026, awareness and uptake are high, but depth of implementation varies. Below is the current landscape:

- Governance and Policies: Nearly all banks and DFIs now have formal structures and policies in place for Green Banking. SBP reported that by late 2022, 100% of banks/DFIs had established Green Banking Offices or units and appointed a Chief Green Banking Manager to supervise sustainability initiatives. Around 79% (31 institutions) had Board-approved Green Banking Policies. Those policies typically include commitments to environmental risk management, green financing promotion, and reducing the bank’s own carbon footprint. We can infer that as of 2026, this number has inched closer to 100% as the remaining banks caught up (especially since SBP has been actively following up). This indicates a sector-wide acceptance of GBG as a norm – having a sustainability policy and some governance structure is now standard practice in Pakistani banking, whereas pre-2017 it was rare.

- Integration of E&S Risk in Credit Processes: A majority of banks have started integrating environmental and social risk checks into their credit appraisal. SBP’s data from 2022 showed 27 banks/DFIs (69%) had included environmental risk assessment in their credit risk procedure. This means when these banks evaluate a loan, they include an E&S risk review (often via an E&S checklist or risk rating) alongside traditional financial analysis. About 46% of banks had set quantifiable targets to reduce their own environmental impact (e.g. energy use, emissions), and 41% had strategies to facilitate green financing (like preferential terms for green projects or dedicated green finance targets). These numbers illustrate that progress is well underway but there is room to grow; roughly one-third of banks were still lagging in systematically managing E&S risk as of 2022. Where banks have indicated that ESRM has been included, it is included to a point of adding a ‘check-list’. How many banks go beyond a routine checklist assessment and implement E&S risk assessment in the spirit is something that still requires strengthening in 2026.

As the ESRM manual rolled out in 2023, banks began upgrading these practices. Through IFC and SBP’s training programs, each bank is nominating personnel to become ESRM trainers and champions. Banks like Habib Bank Limited (HBL) and Bank Alfalah, two of the country’s largest – have been front-runners. HBL, for instance, had implemented an internal Social & Environmental Management System even before the manual, aligning it with IFC Performance Standards, and was actively involved in crafting the GBG. HBL’s policy includes an exclusion list and has made landmark decisions like discontinuing financing of new coal projects since 2020 and pledging to achieve zero coal exposure by 2030. This move, the first of its kind in Pakistan, demonstrates integration of climate transition risk considerations into strategy. HBL recognized the long-term risk (and unacceptability) of coal finance. Other banks have not yet matched this pledge, but Allied Bank and others reportedly conduct environmental impact assessments for large projects and are beginning to set climate-related policies.

Bank Alfalah provides a case of rapid progress with support from development partners. It has adopted SBP’s ESRM framework and aligned with GBG, and in 2023 it signed an advisory agreement with IFC to further bolster its green banking roadmap. With IFC’s help, Bank Alfalah is measuring its environmental and social impacts, exploring green finance opportunities (like green bonds/loans), and training its teams.

- Green Finance Portfolios: On the business side, banks’ green lending and investment is growing, though from a low base. Thanks to SBP’s refinance facility and their own initiatives, banks have financed a significant number of renewable energy projects (solar, wind, hydro). For example, by mid-2022 about 1,600 MW of renewable capacity had been financed across 2,200 projects via banks. This includes utility-scale projects and a large number of distributed solar installations (e.g. rooftop solar for industry and homes). Some banks have carved out niches: JS Bank is notable as it positioned itself strongly in renewable energy financing and was accredited in 2023 as the first Pakistani commercial bank to the Green Climate Fund (GCF). Through GCF accreditation, JS Bank can channel international climate finance into local projects. It has also financed over 385 solar projects for residential and agricultural customers in 2022 and solarized one-third of its branch network. JS Bank’s recognition with a “Green Deal of the Year” award in 2023 gained prominence.

Another instrument gaining traction is green bonds/sukuk. While these have so far been driven by public sector and corporates (e.g. WAPDA’s green bond 2021; a provincial government’s green sukuk; and a recent corporate green sukuk for a hydro project), banks have often been arrangers or investors in these issues. With the PGT in place, banks are expected to both originate more green loans and possibly issue their own green bonds to raise funding for green portfolios. In 2025, Pakistan also saw its first rupee-denominated green bond issued domestically, indicating growing demand for local currency green investment, banks likely played a role in distribution if not issuance. We can anticipate that in their annual reports and sustainability reports, more banks are now disclosing “green financing” volumes (some already do, but definitions varied pre-taxonomy).

- ESG Reporting and Transparency: The push for disclosure is relatively new. SECP’s ESG Reporting Guidelines (voluntary phase) and the forthcoming adoption of IFRS Sustainability Disclosure Standards mean that large banks (most of which are listed companies) will begin reporting climate-related risks and taxonomy-aligned metrics in the coming years. A few leading banks have already issued standalone sustainability or impact reports; HBL publishes an annual Impact and Sustainability report, which details its carbon footprint, green operations, and some portfolio information. It even highlights that HBL helped craft SBP’s GBG and has integrated cross-cutting climate guidelines from its majority owner the Aga Khan Development Network. Meezan Bank, the largest Islamic bank, and MCB have also started to include ESG sections in their reports, often referencing the GBG. However, a 2023 assessment by Fair Finance Pakistan found that public policy disclosures by banks on climate and environment are still generally weak, with low scores on having comprehensive climate strategies or targets (except for HBL’s coal policy). This suggests that while internal actions have started, banks have room to improve on transparent communication and setting measurable public targets (an area likely to improve as reporting guidelines take hold).

- Variation and Industry Culture: There remains a gap between front-runners and others. A few banks have dedicated E&S risk management units with specialists (often those who attended the IFC trainings) and have begun embedding ESG in their culture. For example, progressive banks like HBL, Bank Alfalah, UBL, Soneri Bank and Bank Al-Habib all have a Head of Green Banking, a role that would not have existed a few years ago. These banks treat ESG as part of strategic planning, e.g., considering climate risks in credit portfolio strategy, or marketing themselves as sustainable banks. On the other hand, some smaller or mid-sized banks may still view green banking as a compliance exercise, maintaining the required policy and unit but not yet integrating it fully into business decisions. SBP’s monitoring, through the ESG performance indicators, likely highlights such differences. The good news is that the overall direction is positive. Even reluctant banks are being nudged by peer pressure, regulatory attention, and perhaps reputational concerns to step up. The devastating 2022 floods also served as a wake-up call, making it easier for risk managers in banks to get buy-in from their boards by pointing to tangible examples of climate risk.

- Development Partner Support: Implementation has been bolstered by development partners. Aside from IFC and WWF’s training programs, other institutions like the World Bank, Resources Future, ADB and FCDO have been active. FCDO, for instance, provided support in developing the Green Taxonomy and has issued policy briefs calling for scaling up green finance. The ADB has worked with Pakistan on climate resilience in infrastructure finance through its CDREP program (sub-programs 1 and 20, and one can expect more technical assistance projects to continue. This external support helps ensure Pakistani banks are not alone in figuring out methodologies (e.g. scenario analysis tools, climate risk databases), they can leverage global tools adapted via these partnerships.

Challenges and Next Steps in Implementation

Despite the progress, significant work lies ahead to fully embed GBG, ESRM, and PGT into the fabric of banking operations. The coming years will be crucial for translating policy into practice. Below we outline the key challenges and the expected or recommended next steps in implementation, including guidance, capacity building, supervision, and timelines:

Key Challenges

- Capacity and Expertise: Perhaps the most immediate challenge is the skills gap. Proper ESRM implementation requires trained credit officers, risk managers, and E&S specialists who can identify issues like biodiversity impacts or occupational safety risks in projects. Many banks lack dedicated E&S risk staff and are training existing employees to take on this role. While SBP/IFC’s Train-the-Trainer sessions have helped, continued capacity building is needed to avoid superficial compliance. Banks must invest in developing internal expertise on topics like climate science, environmental law, and social risk – areas traditionally outside core banking. The concept of proportionality must be understood, so staff can apply the right level of diligence (neither too lax nor unnecessarily onerous for low-risk cases). Resources Future has done trainings regularly and has helped banks to speed up green finance roadmap implementations and we continue to look forward to helping banks achieve what best they can.

- Data and Tools: Assessing environmental and social risk, as well as measuring alignment with the taxonomy, requires data that banks often don’t have readily. For example, evaluating a client’s carbon emissions or water usage, or conducting climate stress testing on a portfolio, depends on obtaining quality data. Many borrowers (especially SMEs) in Pakistan do not produce detailed environmental data or disclosures. Similarly, for taxonomy reporting, banks might need to classify thousands of loan accounts – which can be labor-intensive without proper IT systems. The absence of localized risk assessment tools (e.g. models for climate physical risk in Pakistan’s regions) is a constraint. Global banks often rely on global datasets (like NGFS climate scenarios) and then customize them, which is complex.

- Client Awareness and Buy-In: Banks report that some clients are resistant or puzzled when asked for environmental action plans or social compliance documentation. Especially in sectors like textiles or agriculture, clients might view E&S requirements as extra red tape or cost. Changing this mindset is a challenge. For instance, banks have to engage and educate clients that these frameworks can ultimately benefit the client (through risk mitigation and possibly access to green finance). Until borrowers see value (or face pressure from buyers/regulators), banks might encounter pushback, making ESRM implementation more difficult in practice.

- Balancing Growth and Risk Management: Pakistani banks are operating in a tough macroeconomic environment (with recent liquidity and credit risks from economic downturn). There may be a perception that adding E&S filters could slow down business or add costs. Banks might be tempted to treat green banking as secondary when core financial metrics are under strain. Overcoming this short-term trade-off mentality is a challenge; it requires demonstrating that E&S risk management prevents costly problems (e.g., loan defaults due to factory shutdown by environmental regulators) and that green finance can open new profitable markets. In essence, convincing all levels of bank management that “sustainable banking is smart banking” remains a work in progress.

- Ensuring Consistency and Avoiding Greenwashing: As green finance accelerates, there is a risk that in the push to show results, some institutions might label projects as “green” without robust justification. This could be due to misinterpretation of the taxonomy or deliberate overstatement. Such greenwashing would undermine trust in these frameworks. Ensuring strict adherence to PGT criteria and verification of claims is a challenge.

- Technical Complexity – Climate Risk Quantification: A forthcoming challenge is the more advanced climate risk techniques like scenario analysis and stress testing. SBP has dabbled in macro-level climate stress tests, but expecting individual banks to run climate stress scenarios on their portfolios is a big step. It involves modeling how extreme floods or carbon taxes, for example, would impact credit risk metrics. Many banks find this technically daunting. Similarly, aligning with TCFD recommendations (Task Force on Climate-related Financial Disclosures), such as estimating how a 2°C scenario affects their business, is complex and often model heavy. Such an expertise is also not available in Pakistan. Overcoming this will require industry-wide collaboration, shared methodologies, and perhaps centralized scenario guidance from SBP or NGFS.

- Policy Coherence and Incentives: Last, there is a challenge is ensuring that other policies (fiscal, energy, industrial) support the green banking objectives. If, for instance, fossil fuel subsidies remain high or environmental regulation on companies is weak, banks’ efforts to be green can only do so much. A supportive policy environment (like carbon pricing or enforceable environmental standards) enhances the business case for green projects. While this is beyond banks’ control, it’s a contextual challenge. Internally, banks also need to align their incentive structures, credit officers and relationship managers should have performance metrics that value E&S quality, not just volume of lending. If staff are only rewarded on short-term loan growth, they may ignore E&S risks or avoid green projects that take longer to appraise. Shifting incentive structures and credit culture is a delicate task ahead.