Introduction

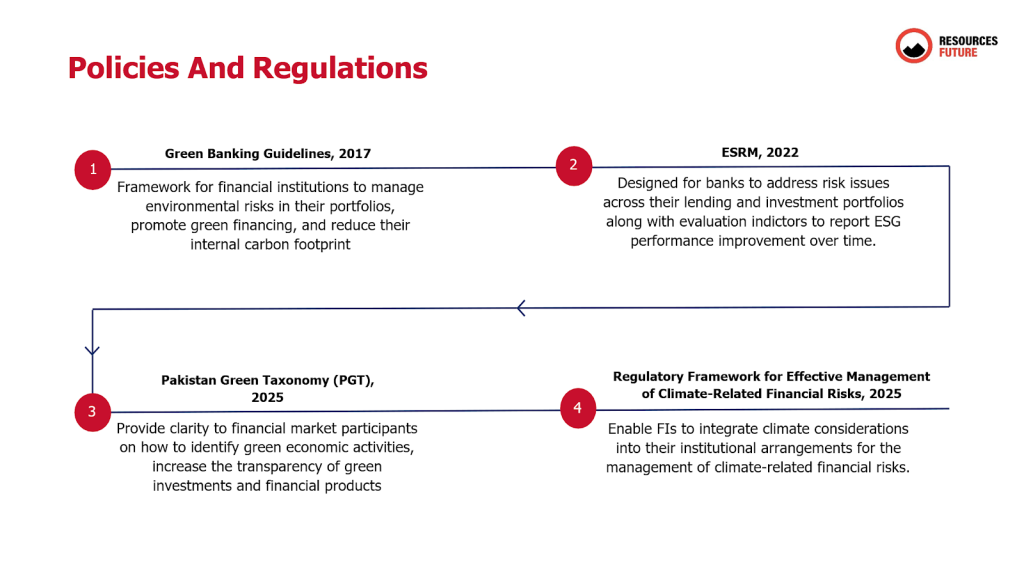

Pakistan’s financial sector is increasingly recognizing that environmental and social sustainability is integral to long-term stability. The country’s acute vulnerability to climate change, evidenced by over 150 extreme events in the past 25 years and catastrophic floods in 2022 and 2025, have underscored the need for banks to manage environmental and social (E&S) risks and support climate-resilient growth. In response, the State Bank of Pakistan (SBP) and other institutions have introduced a set of four frameworks to steer the banking industry towards sustainable practices: the Green Banking Guidelines (GBG), the Environmental and Social Risk Management (ESRM) framework, Pakistan Green Taxonomy (PGT) and Regulatory Framework for Effective Management of Climate Related Financial Risks. These initiatives aim to embed environmental & social considerations into banks’ risk management, strategy, and reporting. This briefing note explains each framework’s definition, objectives, and context; traces their regulatory evolution (including global influences) and examines how they complement each other. Subsequently, we will also assess the current state of implementation; and outlines next steps and challenges for moving from policy to practice. RF’s goal is to provide readers, SBP, and development partners with a clear, nuanced understanding of what these frameworks are and how to implement them effectively.

Green Banking Guidelines (GBG) – Definition, Objectives, and Context

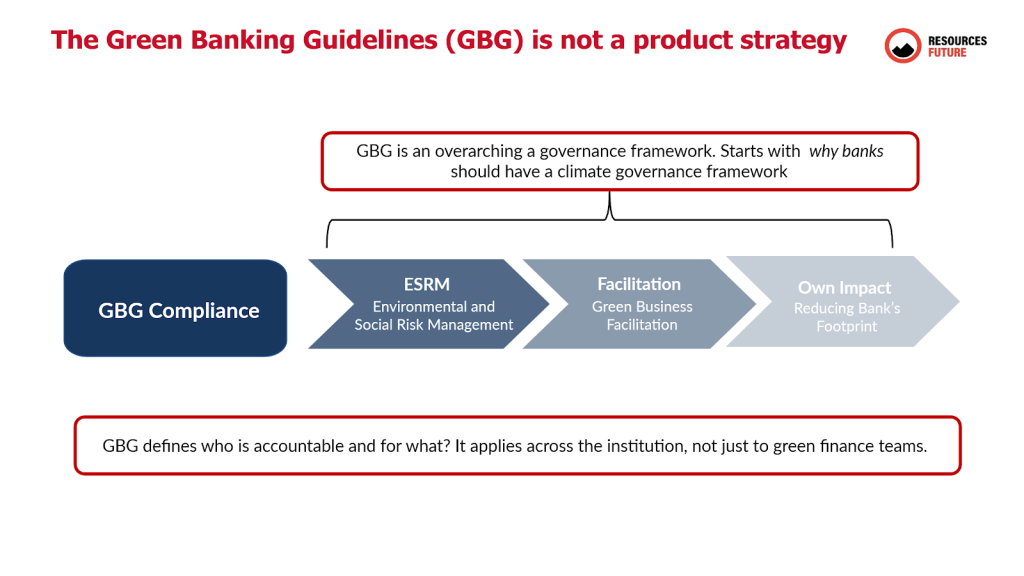

The Green Banking Guidelines (GBG) are a set of guidelines issued by the SBP in October 2017 as a foundational step to integrate sustainability into Pakistan’s banking sector. SBP introduced the GBG via IH&SMEFD Circular No. 08 of 2017 with three broad areas of focus:

Own Impact Reduction: Reducing the bank’s internal environmental footprint (e.g. energy, water, paper usage) and improving social practices within their operations. This includes measures like adopting energy-efficient technologies in branches, reducing waste, and improving labor and community practices. The aim is for banks to “lead by example” in sustainability.

Risk Management: Strengthening financial stability by identifying, managing, and mitigating the environmental risks in banks’ portfolios. This means banks must consider how issues like pollution, climate change, or environmental non-compliance by borrowers could translate into credit or operational risks, and take steps to reduce potential losses. Essentially, GBG encourages forward-looking risk assessments so that environmental and social risks do not later manifest as financial losses.

Green Business Facilitation: Proactively increasing financing to environmentally sustainable (“green”) sectors and projects. The guidelines nudge banks to tap into emerging opportunities such as renewable energy, energy efficiency, clean transportation, and other “green” projects. SBP saw this as a way to augment banks’ profitability by financing relatively untapped yet viable projects that are environmentally compliant and socially responsible.

The GBG’s overarching objectives were to protect banks from environment-related risks. SBP explicitly noted that while borrowers themselves bear primary responsibility for complying with environmental laws, the GBG would help banks avoid losses by managing the environmental vulnerability of their lending portfolios. At the same time, the guidelines seek to push banks to fulfill their environmental responsibilities (as corporate citizens) and ensure financing is available for Pakistan’s transition to a resource-efficient, climate-resilient economy. This dual aim of risk reduction and positive impact runs through the GBG.

The GBG came on the heels of SBP joining the International Finance Corporation (IFC)’s Sustainable Banking and Finance Network (SBFN) in 2015. SBP’s motivation was reinforced by Pakistan’s national climate commitments and the increasing global focus on green finance. The GBG can be seen as SBP’s first formal step to green the financial system, aligning with what regulators in countries like Bangladesh, China, and Indonesia were already doing. SBP expected banks/DFIs to implement the GBG within one year (i.e. by late 2018). To facilitate this, SBP committed to monitor progress, conduct trainings, and provide other support.

The GBG themselves (detailed in an SBP booklet) outline specific actions such as: developing a board-approved Green Banking Policy covering risk assessment procedures and green business promotion; setting up a Green Banking Unit or designating officials to oversee implementation; integrating environmental risk criteria into credit approval processes; maintaining an exclusion list of prohibited environmentally harmful activities; tracking and reducing the bank’s own resource consumption; and periodically reporting progress to SBP. The guidelines emphasize that high-level governance is crucial, bank boards and senior management are expected to champion these initiatives. By 2017, GBG provided a common framework and signaled regulatory priority on sustainability.

Environmental and Social Risk Management (ESRM) Framework – Definition and Objectives

The ESRM framework in Pakistan refers to the processes and standards that banks use to identify and manage environmental and social risks in their lending and investment activities. While the GBG laid out the expectation for banks to integrate E&S risk in credit decisions, the ESRM Framework (embodied in an ESRM Implementation Manual issued by SBP) provides the concrete methodology and tools to do so. In November 2022, SBP, with IFC’s assistance, launched a comprehensive ESRM Manual for Banks and DFIs. This manual operationalizes the risk management pillar of GBG by setting standardized guidelines on how banks should screen transactions for E&S issues, categorize risk levels, conduct due diligence, and monitor E&S performance over the life of a loan.

At its core, ESRM is about integrating E&S risk considerations into the overall credit risk management process. This means before a bank approves financing, it should evaluate how the borrower’s activities could negatively impact the environment or society, and conversely how environmental or social factors (like climate change or labor issues) could impair the borrower’s ability to repay. The ESRM framework typically includes: an Environmental and Social Management System (ESMS) (a set of policies/procedures within the bank), E&S risk categorization (classifying loans as high, medium, or low E&S risk), due diligence processes (e.g. site visits, E&S action plans for clients), and monitoring and reporting mechanisms. In Pakistan’s case, the ESRM was pioneering in providing local banks with user-friendly tools and checklists for these tasks. It is aligned with international standards, drawing especially from the IFC’s Performance Standards and the Equator Principles, which are globally recognized benchmarks for E&S risk management in finance.

The ESRM framework’s primary objective is to reduce banks’ exposure to losses by proactively managing environmental and social risks in their portfolios. By screening out or mitigating high E&S risks, banks can avoid credit defaults, legal liabilities (e.g. fines for environmental violations), and reputational damage. A second key objective is to standardize practices across the industry. Prior to the ESRM manual, banks had uneven approaches, some had rudimentary checklists, others none, and no common benchmark existed for what constituted adequate E&S due diligence. The new framework establishes minimum standards and benchmarks so that all banks at least cover the basics of E&S risk evaluation. Importantly, the ESRM framework in Pakistan explicitly covers social risks in addition to environmental risks. This means issues like labor rights (e.g. child labor, forced labor), community health and safety, land acquisition, impacts on indigenous peoples, etc., are within scope now.

SBP developed the ESRM Implementation Manual in partnership with IFC. The manual was rolled out at a high-profile Sustainable Banking Conference in November 2022, chaired by SBP’s Governor with all bank CEOs present. SBP opted to make adoption of the ESRM manual voluntary for an initial 3-year period. During 2023–2025, banks are expected to gradually integrate ESRM into their credit processes, with SBP monitoring progress and providing support. Two banks volunteered to pilot the manual on a fast-track basis as a learning exercise for the rest. After this phase, it is anticipated (though not explicitly stated in the 2022 announcement) that aspects of ESRM may become mandatory or part of regular supervisory expectations. The SBP has started quarterly monitoring of ESRM implementation status at banks/DFIs.

Overall, Pakistan’s ESRM framework is aligned with global standards. The IFC Performance Standards (a widely used E&S risk management benchmark for project finance) form a backbone, the manual and training modules explicitly cover IFC’s standards and other international norms. This ensures Pakistani banks are meeting the kind of E&S criteria that international lenders and investors expect. The concept of categorizing projects as High, Medium, Low risk and conducting due diligence commensurate with risk (“proportionality”) also comes from IFC and Equator Principles practices.

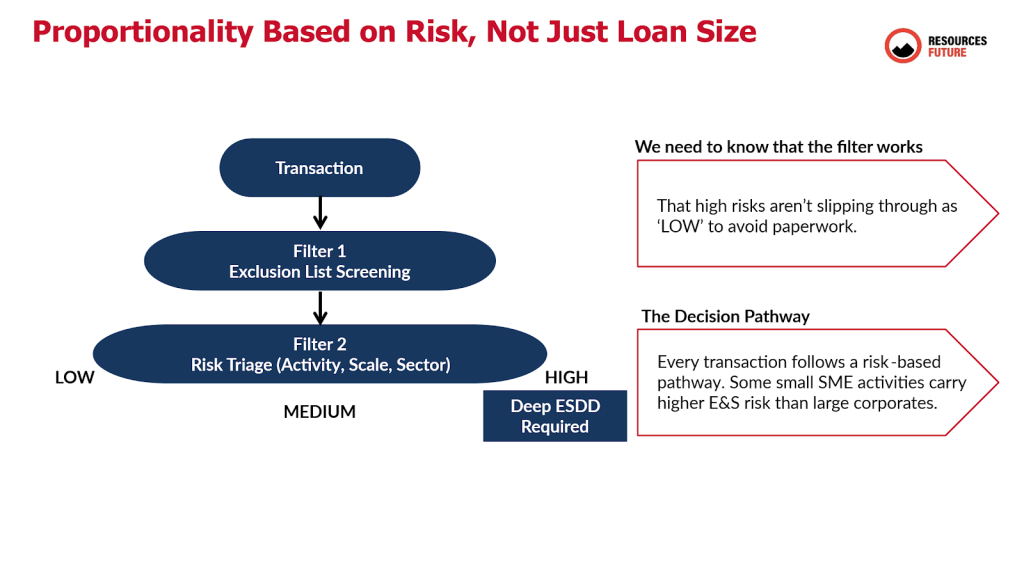

In the figure above, the “Transaction” box at the top is deliberate. ESRM is not a ESG side process. It is meant to be embedded in credit workflow (origination → appraisal → approval → documentation → monitoring). The implication for operationalization is that no transaction should proceed to approval without an ESRM decision stamp (even if that stamp is “Low risk – standard controls only”).

Filter 1 is the non-negotiable gate. Exclusion list screening answers: Is this transaction categorically unacceptable for the bank, regardless of profitability or collateral?

The exclusion list typically includes activities that present unacceptable legal/regulatory exposure, severe environmental harm, egregious social harms (e.g., forced/child labor), or prohibited products and practices. The logic is important: exclusion lists are not a risk rating tool; they are a “no-go” tool. If an activity triggers the exclusion list, the pathway should terminate or require explicit exception governance at the highest level (and in mature systems, exceptions are rare and time-bound).

Filter 2: Risk triage (activity, scale, sector) – the proportionality engine

Once a transaction passes the exclusion list, it enters Filter 2, which is the core of the slide: risk triage. The triage explicitly uses risk drivers, not loan amount:

(a) Activity risk

What is the client actually doing with the funds? Same borrower, different use-of-proceeds can mean different risk. For example:

- “Textile company” is not sufficient, dyeing/finishing has very different risk from garment stitching.

- “Agriculture SME” is not sufficient, pesticide handling, water extraction, labor conditions, and land-use change determine the risk.

(b) Scale and footprint

Scale affects the severity and spread of impacts. Small scale does not mean low risk, but it can influence whether risks are localized and manageable or systemic. Scale includes:

- Production capacity, geographic footprint, proximity to sensitive receptors (water bodies, schools, settlements)

- Volume of effluent/emissions/waste

- Intensity of labor use and subcontracting

(c) Sector context (and maturity of controls)

Sector risk is not only “what the sector is,” but how regulated and controlled it is. Some sectors in Pakistan are known for compliance variability (environmental permitting, wastewater disposal, informal labor). A bank’s triage should consider:

- Typical compliance issues in the sector

- Whether environmental approvals are routinely obtained/enforced

- Known hotspot risks (e.g., groundwater stress, hazardous waste)

Output: Low / Medium / High

This is the decision point that sets the level of due diligence and monitoring. The slide’s left-to-right “LOW → MEDIUM → HIGH” conveys a gradient: as risk increases, documentation, due diligence depth, and governance requirements escalate.

Pakistan Green Taxonomy (PGT) – Definition, Objectives, and Scope

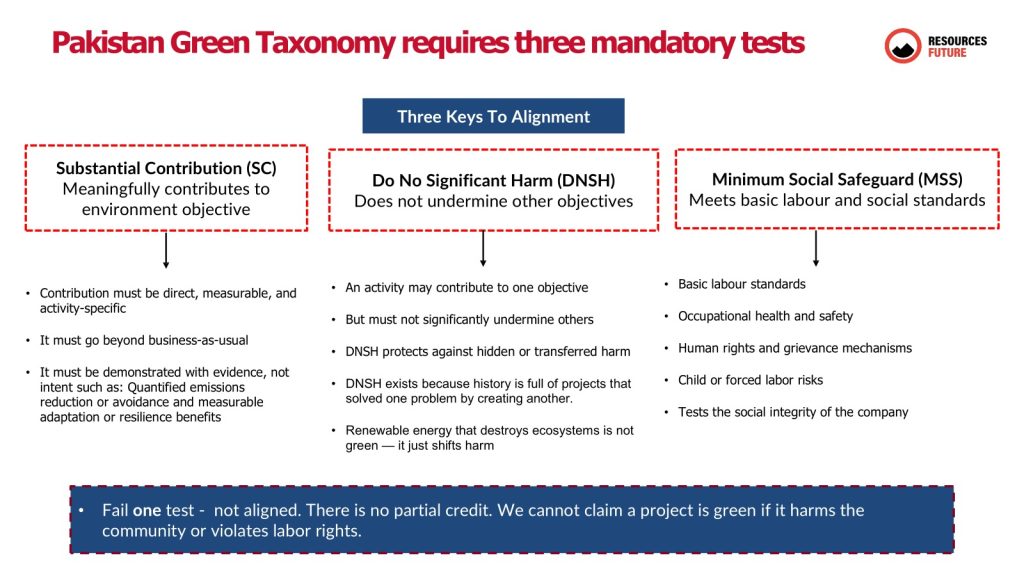

The PGT is an official classification system that defines what economic activities and assets qualify as “green” or environmentally sustainable in the Pakistani context. Launched by the Government of Pakistan (with collaboration between the Ministry of Climate Change, SBP, and the Securities & Exchange Commission of Pakistan), the PGT provides a single, science-based definition of ‘green’ to be used across the financial sector. In practical terms, the taxonomy lists specific sectors, sub-sectors, and project types that contribute substantially to environmental objectives such as climate change mitigation, climate adaptation, pollution reduction, sustainable water management, biodiversity conservation, etc., along with criteria or thresholds for each. By doing so, it creates a common language for green financing, for example, whether a given renewable energy project, energy-efficient building, or sustainable agriculture practice is considered “green” under national standards.

The 2025 PGT identifies activities in priority sectors with substantial contributions to climate change mitigation (6 sectors) and climate change adaptation (8 sectors). For mitigation, sectors include renewable energy, energy efficiency, low-carbon transport, green buildings, waste management, and industrial processes that reduce emissions. For adaptation, sectors include climate-smart agriculture, water management, disaster risk reduction, resilient infrastructure, etc. Notably, the PGT also took a “multi-objective” approach for certain sectors like agriculture, forestry, fisheries, and tourism. In those sectors, an activity might qualify if it supports not just climate objectives but also other environmental goals like healthy ecosystems or biodiversity.

Crucially, the PGT embeds the principles of “Do No Significant Harm” (DNSH) to other environmental objectives and adherence to minimum social safeguards. In other words, for an activity to be labeled green, it must not seriously harm other environmental goals (for example, a hydroelectric project should not destroy critical wildlife habitat) and it must respect basic social standards (no forced labor, respecting community rights, etc.). These requirements mirror the EU Taxonomy’s framework of Substantial Contribution + DNSH + Social Safeguards, indicating strong influence from global best practices. By incorporating these nuances, PGT ensures that “green” in Pakistan is not just about one narrow benefit but about overall sustainability.

The PGT is about defining the “what” of green finance. It complements the process-focused GBG and ESRM by providing content criteria. It reflects lessons from the EU Taxonomy and China’s Green Taxonomy, adapted to national priorities (e.g., Pakistan’s climate targets per its NDC, and key sectors like agriculture and tourism). It will likely be updated periodically (“2025 edition” implies future editions) as technologies evolve or new priorities emerge.